With about 83 percent of Americans who follow a budget saying rising costs are their biggest challenge, the personal finance company WalletHub recently released its report on 2026’s Cities With the Best and Worst Budgeters. The study highlights the places where residents are managing their finances most effectively, while also pointing to areas that have room for improvement.

To identify where the best budgeters live, WalletHub compared more than 180 U.S. cities across 12 key metrics, including average credit scores, debt-to-income ratios, and foreclosure rates.

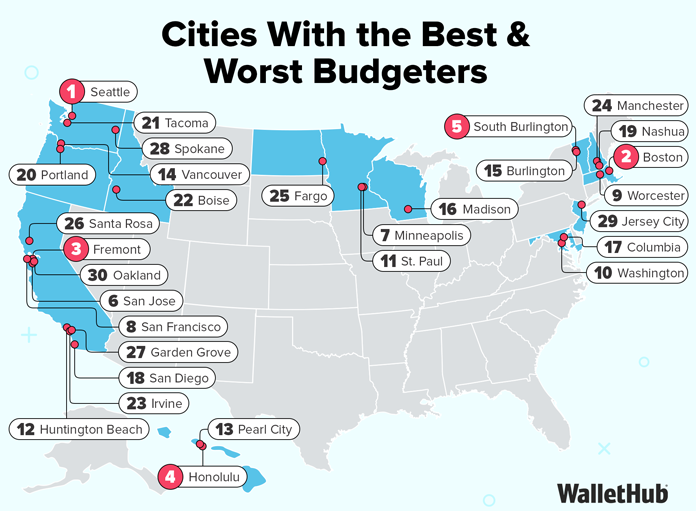

Three California cities made the ‘top ten’ in having the best budgeters based on the study.

Cities with the Best Budgeters

Seattle, Washington took the top spot as the city with the best budgeters, followed by Boston, MA; Fremont, CA; Honolulu, HI; South Burlington, VT; San Jose, CA; Minneapolis, MN; San Francisco, CA; Worcester, MA; and, at number 10, Washington, DC.

Cities with the Worst Budgeters

Those at the bottom of the list included Memphis, Tennessee at number 173, followed by Mobile, AL; North Las Vegas, NV; New Orleans, LA; Montgomery, AL; Huntington, WV; Charleston, WV; Shreveport, LA; Jackson, MS and, at number 182, last on the list, Gulfport Mississippi.

“Creating a budget is essential because it helps you avoid overspending and enables you to meet your financial goals like paying off debt, building an emergency fund or saving for retirement. Budgeting can also improve your credit score by helping you develop responsible financial habits, and can make it easier to catch fraud,” WalletHub Analyst Chip Lupo said. “Seattle has the best budgeters in the U.S., with residents having some of the lowest debt-to-income ratios in the U.S. for credit card debt, student loan debt and car loan debt. Seattle residents also have one of the lowest credit utilization ratios in the country, with residents using around 37 percent of their credit limits, on average. This is very close to 30 percent, the recommended maximum credit utilization ratio. Another way people in Seattle show their ability to stick to a budget is the fact that they have one of the lowest 90-day mortgage delinquency rates in the country.”

To view the full report, visit: https://wallethub.com/edu/cities-with-best-worst-budgeters/7666/

Expert Commentary

What is the biggest obstacle for consumers trying to stick to their budgets?

“Keeping up with the joneses has always been one of the toughest challenges for disciplined personal finance. As income increases, people tend to proportionally increase spending rather than saving more. The pressure to keep up with peers’ visible spending (newer cars, homes, vacations) can derail even well-intentioned budgets. The next obstacle is job loss or other emergencies that can come at someone. However, this is why adhering to a budget and having savings for rainy days matter. However, the psychological difficulty of delaying gratification in a culture built around instant satisfaction does pose a significant challenge, especially now as people live on social media.”

Dr. Suchi Mishra – Professor, Florida International University

“Research shows that consumers also regularly underestimate small, unplanned purchases. For example, when going to the grocery store, people almost always pick up a few items that are not on their usual list – such as buying a nicer olive oil for a specific dish or realizing they are out of dishwasher tabs and choosing the largest box to save on cost per tab. Because of this, when budgeting it is important to do what some people call ‘planning for unplanned purchases.’ Just as with large projects, it helps to build in a margin of error. Figure out what a normal grocery bill looks like and budget an extra 10 percent. Decide how much is reasonable to spend on a day out at an amusement park and add $20. However people approach it, budgeting for these small, everyday extras makes it much more likely that they will stay within their overall budget, rather than only accounting for large monthly or yearly expenses.”

Helen Colby, Ph.D. – Assistant Professor, Indiana University

How should parents teach children about the importance of budgeting?

“Make teaching budgeting concrete, age-appropriate and fun. Letting them have some consequences is critical. Overspending can lead to losing a privilege whereas savings can result in a nice reward. Let them participate in family spending decisions. Model good behavior openly. Discuss family budgeting decisions in front of children. For example, vacation planning can involve kids in deciding flight vs. drive, type of flight, hotel and food etc. They will be excited to participate. Give them responsibility by giving small allowances for discretionary spending, then gradually expand to clothing budgets, phone bills, or car expenses as they prove they can handle it. The goal is to help them understand that money is finite, choices have tradeoffs, and intentional decisions lead to better outcomes than reactive spending. When kids grow into teens they can have a debit card with a limit. Nowadays there are options to get free checking accounts with debit cards and options to lock the card, etc.”

Dr. Suchi Mishra – Professor, Florida International University

“Parents are children’s primary financial educators, yet money remains one of the least discussed topics in many households. Starting financial education early creates lifelong habits. For young children (ages 3-7), use transparent jars instead of piggy banks so they can see money accumulate. Introduce basic concepts like waiting to buy something they want. Teach kids about delayed gratification and the joy that comes from anticipation. Give them small amounts to manage and let them make mistakes with low stakes. For older children (ages 8-12), introduce the concept of earning through age-appropriate chores, distinguishing between expected contributions to the household and extra tasks. Help them divide money into spending, saving, and giving categories. Studies show that children who learn to allocate money to different purposes develop better financial habits as adults. For teenagers, open a checking account together and teach them to track transactions. Involve them in family budgeting discussions, showing how household expenses work. Let them earn larger amounts and make bigger decisions, including mistakes. A teenager who spends their entire summer earnings impulsively learns a more valuable lesson than one whose parents always rescue them. Model healthy financial behavior. Children absorb attitudes about money from watching parents more than from lectures. Discussing family financial goals, demonstrating comparison shopping, and showing contentment with what you have will teach more powerfully than any allowance system.”

Yoav Wachsman – Professor, Coastal Carolina University

Tips for Better Budgeting

You’re more likely to succeed and stay on track if you have a solid plan. The budgeting process involves gathering information about your finances, setting goals for what you want to accomplish, allocating money based on how essential each expense is and tracking your progress.

You can take advantage of online budgeting tools to build your ideal budget, whether you prefer to micromanage every expense or just create a few general categories.

Your monthly debt payoff should be your first priority. Then comes essential expenses, like bills, groceries, and gas, along with saving money for the future. Only after these things are taken care of should you allocate money for “wants.”

Track your spending on a daily basis so you constantly know your progress, or just sync your bank accounts and credit cards with a budgeting app. In addition, keep your long-term budget goals written down in a place where you’ll see them often, and partner with a family member or friend to hold each other accountable.